Chapter 5 — What Can Be Done

The four prior chapters described Stockbridge’s structural condition. Who lives here. What the town owns. How it got to this configuration. What the Commonwealth’s 2024 designation recognizes. This chapter turns from diagnosis to operation. The Town has fiscal levers and statutory tools the prior chapters’ findings make consequential. Each one is presented here with its mechanics, its Stockbridge-specific numbers, and its trade-offs. The decisions are the Town’s to make. The chapter’s task is to make the decisions legible.

Section A — Fiscal Tools

Four fiscal levers are available to Stockbridge. Three are not contingent on the Seasonal Community designation. The fourth — the §5C residential exemption at its expanded ceiling — requires designation acceptance.

Compliance recovery across four independent streams

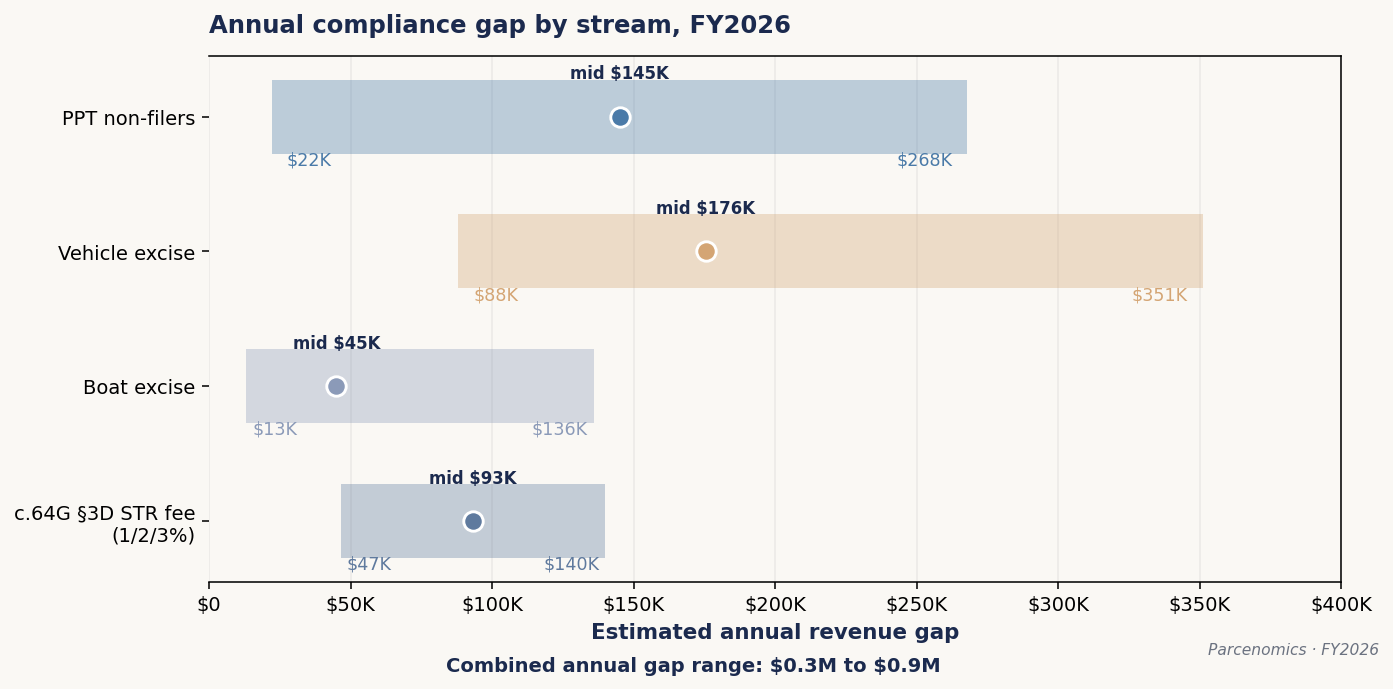

Compliance recovery is the recovery of revenue the Town is statutorily owed but does not currently collect, because the underlying tax obligations are either under-reported or not reported at all. Four streams have been examined in detail for Stockbridge.1

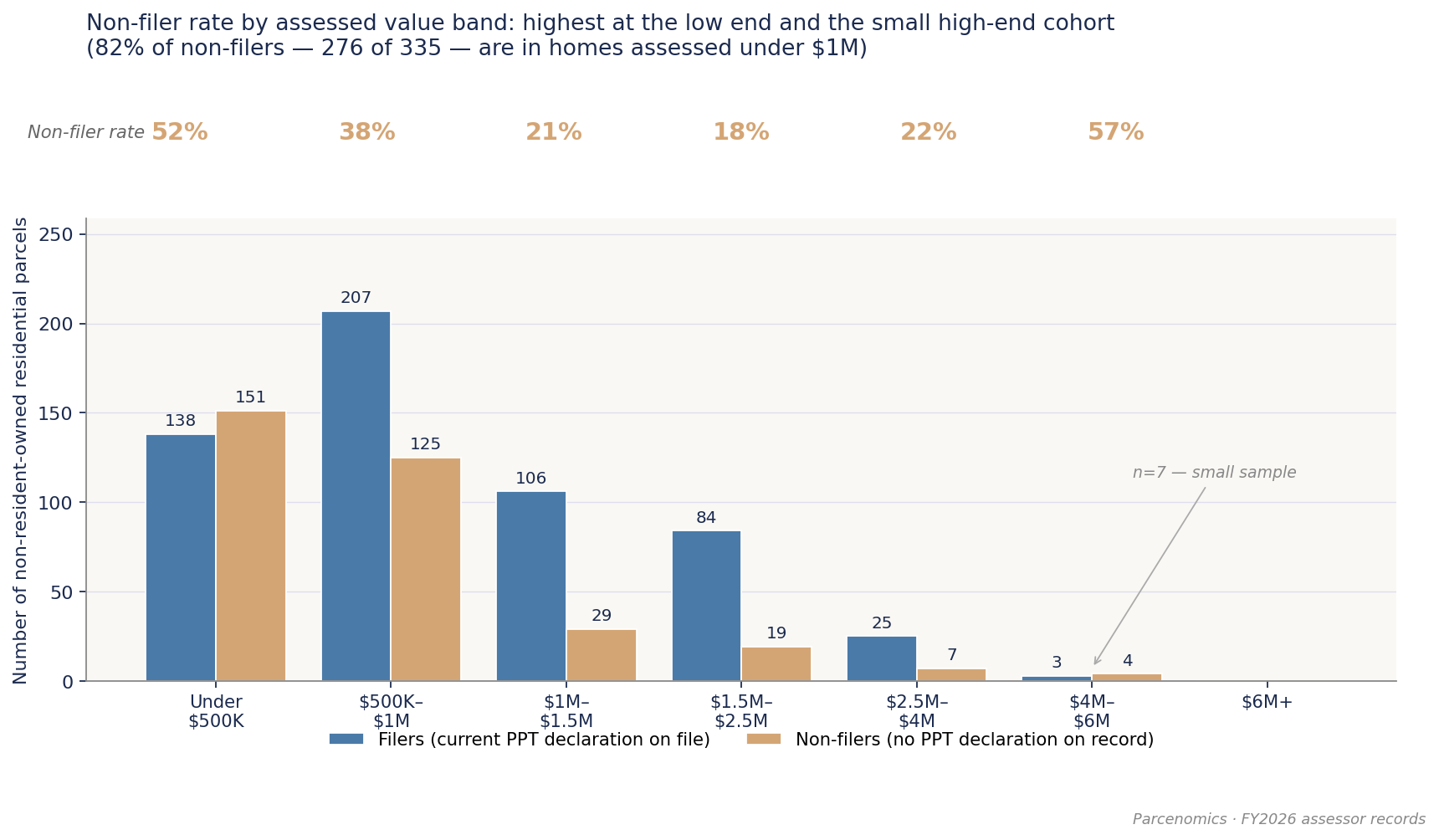

Personal property tax on second-home furnishings. Owners of second homes in Stockbridge are required by statute to file an annual return listing the assessed value of furniture, equipment, and other tangible personal property kept at the home. The town’s analysis identifies a strict universe of approximately 247 second-home parcels with no Personal Property Tax return on file — parcels whose non-resident classification is supported with high or medium confidence by the residency tier model and whose owners do not appear on the FY2026 personal property roll. Estimated annual revenue from this stream is approximately $134,000 under a conservative 50%-recovery assumption against an insurance-replacement contents-valuation benchmark; full recovery against the same benchmark would yield approximately $268,000. Approximately 24 additional parcels were excluded from the strict universe because their residency could not be classified with confidence — the contested-signal and unresolved entity-owned cohorts; some of these are likely non-compliant and would surface as additional non-filers through subsequent data acquisition (LLC manager unmask, additional voter rolls). The strict universe represents a floor on the non-filer cohort, not a point estimate.2

Vehicle excise on Stockbridge-garaged vehicles. Motor vehicle excise is owed in the municipality where a vehicle is principally garaged. Vehicles owned by Stockbridge property owners but registered elsewhere — typically at the owner’s out-of-town primary residence — are not currently producing excise revenue for Stockbridge. The analysis identifies approximately 117 non-resident-owned parcels where a Stockbridge-garaging claim is plausible based on use patterns. Estimated annual revenue gap: $88,000 to $351,000.3

Boat excise on Stockbridge-moored boats. Boats moored or kept in Stockbridge waters are subject to excise tax regardless of where the owner lives. The analysis identifies approximately 452 parcels with mooring or storage signals where no boat excise filing is on record. Estimated annual revenue gap: $13,000 to $136,000.4

Short-term rental community impact fee under M.G.L. c.64G §3D. Massachusetts allows municipalities to impose a community impact fee of up to 3 percent on professionally-managed short-term rental units under M.G.L. c.64G §3D(a). A separate vote under §3D(b) could extend the fee to owner-occupied two- and three-family dwellings operating as STRs; that option is dependent on first adopting §3D(a). Stockbridge has not adopted this fee — the FY2026 Tax Rate Recapitulation shows $0 in community-impact-fee receipts. Estimated annual revenue at three potential adoption rates: $47,000 (1%), $93,000 (2%), $140,000 (3%).5 If adopted, M.G.L. c.64G §3D(c) requires that at least 35 percent of community impact fee receipts be dedicated to affordable housing or local infrastructure projects. The remaining 65 percent is unrestricted and flows to the general fund. The statute does not require receipts to be tied to costs caused by short-term rentals; the only spending restriction is the 35 percent earmark.

The combined annual gap across the four streams, ranging across conservative and aggressive recovery assumptions on the strict universe, totals roughly $0.3 million to $0.9 million. This is a floor on the recoverable gap; parcels excluded for classification uncertainty include some likely non-compliant cases that would surface through outreach and subsequent data acquisition.

The methodology behind each stream’s gap estimate, the parcel-level outreach candidates the analysis produced, and the recovery-rate assumptions are documented in the Technical Appendix. The point for this chapter is that each stream is a real lever the Town can activate. Compliance recovery has not historically been pursued as a systematic program in Stockbridge. Doing so requires letters to identified non-filers and follow-up administration. It does not require a new statute, a new ordinance, or a Town Meeting vote.

Time-lag in the non-resident-owned residential base

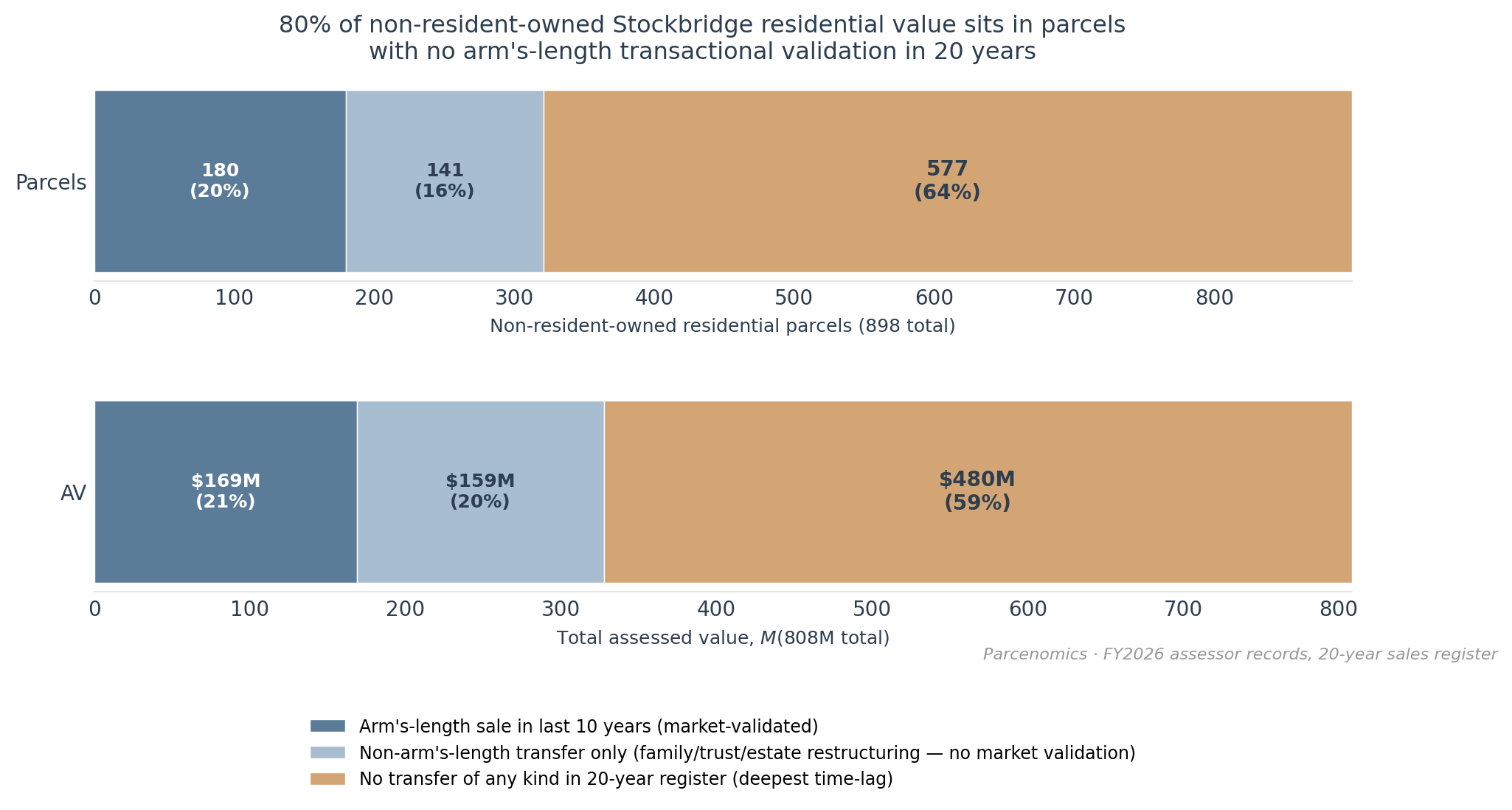

The compliance recovery framework described above addresses non-filers — parcels with no Personal Property Tax declaration on record. A broader structural question concerns the relationship between the current market value of non-resident-owned residential property and the assessment-and-declaration basis on which it is currently taxed. The Chapter 2 finding of an FY2026 implied assessment-to-sale ratio of 114.1% measures the aggregate effect of assessment lag at the municipal level. The parcel-level reality is more concentrated and analytically consequential.

Of the 898 non-resident-owned residential parcels in Stockbridge, carrying $808 million in assessed value, only 180 parcels (20%, $169 million) have transacted at arm’s length in the past ten years. These parcels have a recent market-price validation point against which the assessor’s estimate can be calibrated. The remaining 718 parcels — 80% of the non-resident cohort, carrying $639 million in assessed value — have no arm’s-length transactional anchor in the 20-year sales register.6

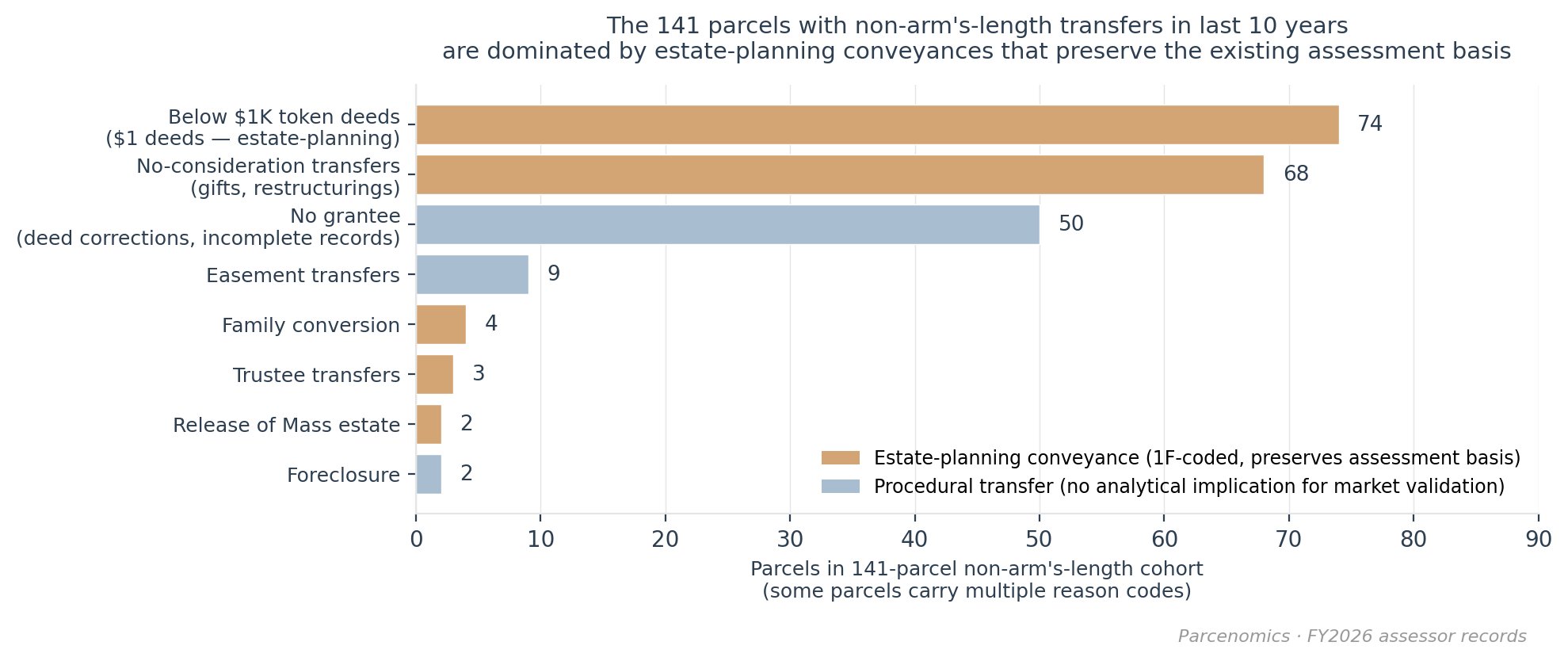

The 718 parcels with no arm’s-length anchor stratify further into two distinct mechanisms producing the same effect. 577 parcels ($480 million, 59% of non-resident-owned AV) have no transfer of any kind recorded in the 20-year register. These are parcels held by the same ownership across two decades, never appearing in the assessor’s transactional record. The remaining 141 parcels ($159 million, 20% of AV) have had non-arm’s-length transfers recorded but no market transactions. The non-arm’s-length transfers are predominantly estate-planning conveyances. Validity-code flags on the 141 parcels overlap — a single deed can carry both a below-$1K consideration flag and a zero-consideration flag — so the category counts are not mutually exclusive: 74 parcels carry below-$1K token-deed flags, 68 carry zero-consideration flags, with smaller flag counts on family conversions, trustee transfers, and estate releases. 128 of the 141 carry the Massachusetts Department of Revenue’s 1F validity code — “family / no consideration.” These transfers move parcels between family members or trust vehicles without producing a market-price validation point, leaving the underlying assessment basis intact across the transfer.

For both mechanisms, the structural result is the same: the assessment estimate has been carried forward through biennial Equalized Valuation cycles and market-trend overlays for a decade or more without an arm’s-length sale price to validate against. In a market that has experienced substantial appreciation — particularly for residential property in resort communities since 2020 — the gap between current market value and the carried-forward assessment grows with each year that passes without a transactional validation point.

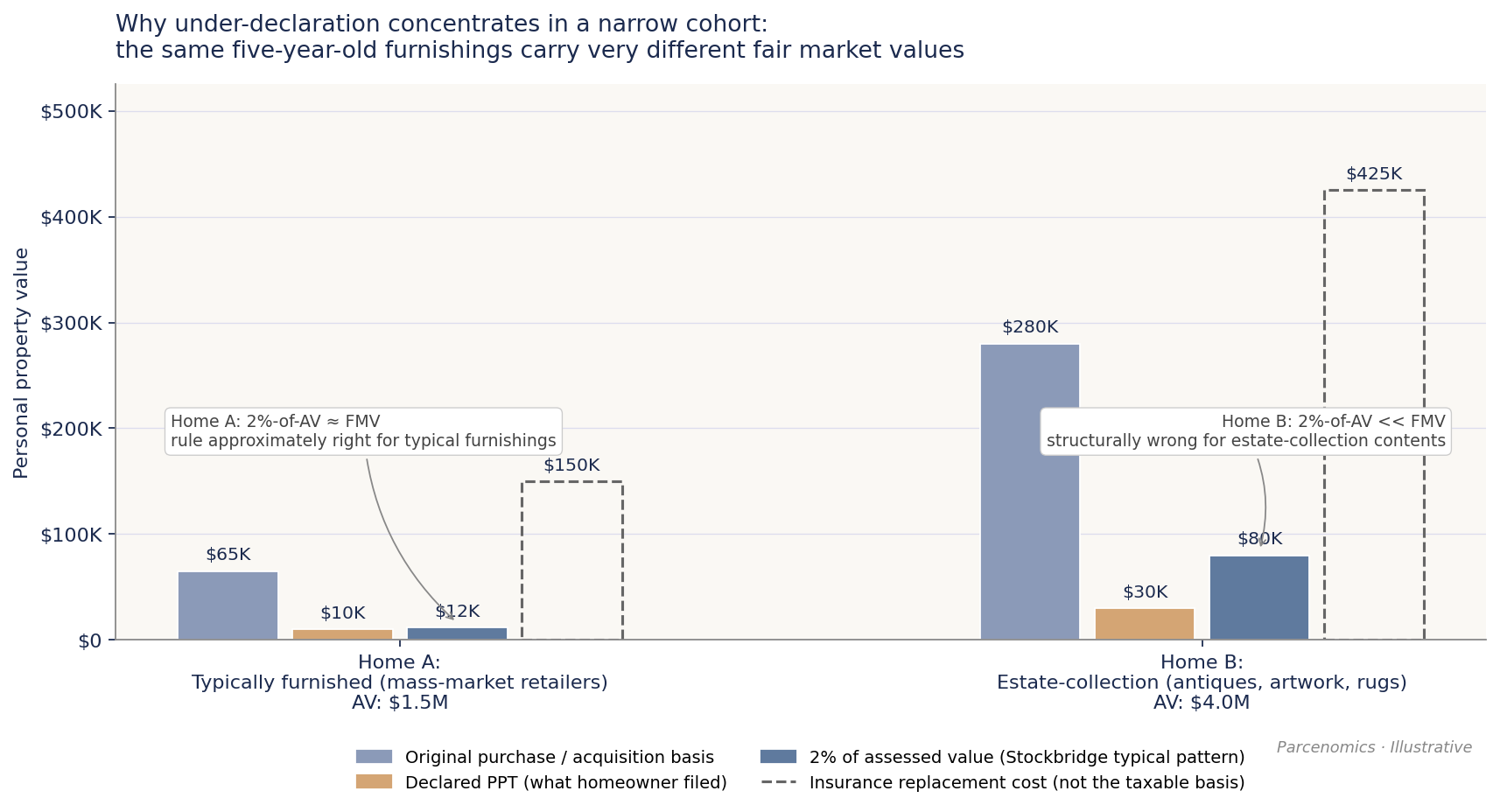

Personal property tax declarations on these same parcels exhibit a parallel structural pattern. Massachusetts personal property is filed annually under M.G.L. c.59 §5 Cl.20 via Form of List, but the practical reality is that declarations are typically filed once, at the time of property acquisition or initial declaration, and carried forward year-over-year with minimal change. The assessor does not typically force annual updates absent specific challenge. Parcel-level quantification of how long Stockbridge declarations have remained unchanged is not available from the current ingestion, but the structural argument applies: declarations filed at the time of property acquisition carry forward without recalibration triggers, growing further from current contents fair market value over the same window.

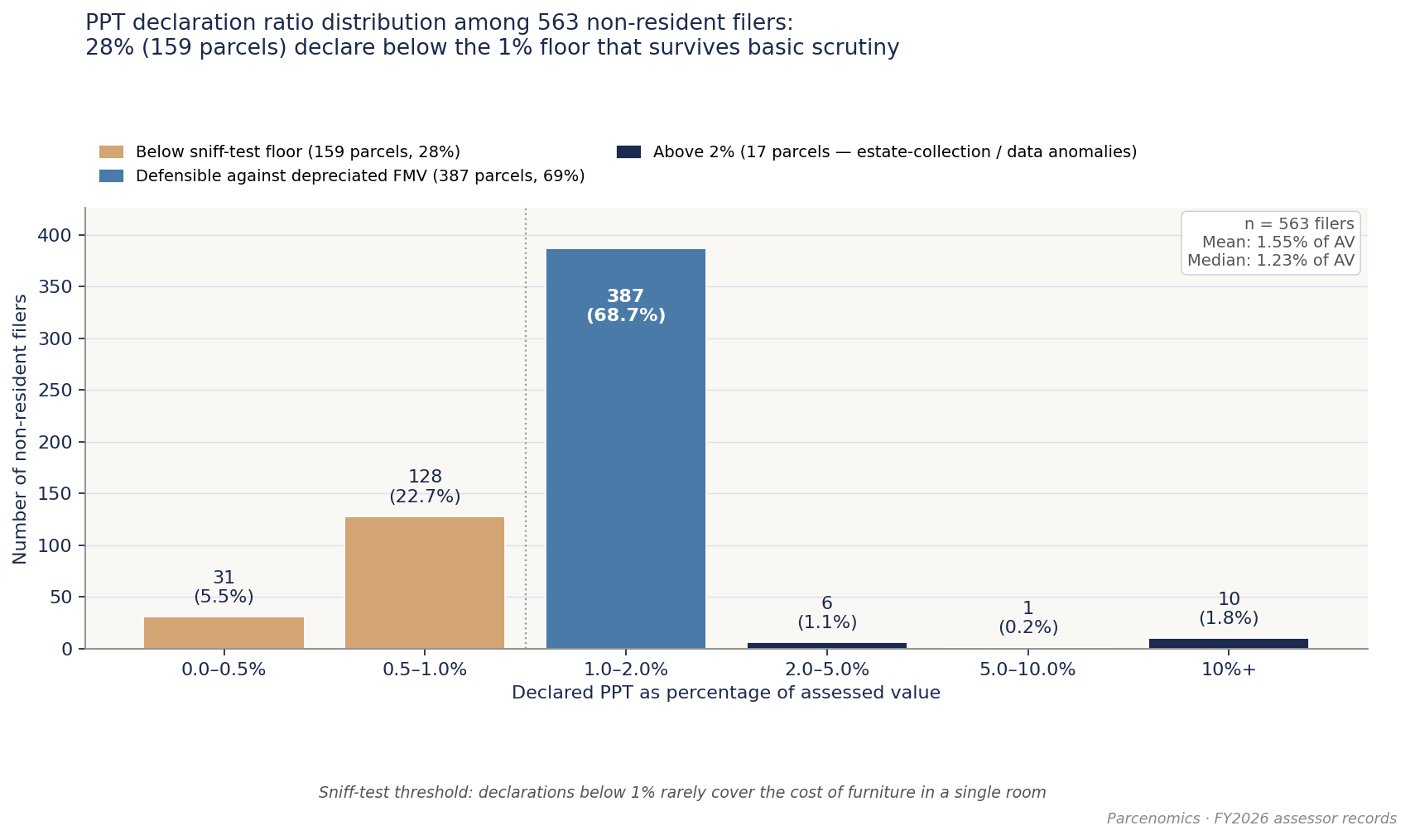

The empirical pattern in current Stockbridge declarations is consistent with this structural argument. Across the 563 non-resident filers with current declarations on record, the mean PPT-to-AV ratio is 1.55% and the median is 1.23%. The bulk of filers (387 parcels, 69%) cluster in the 1.0%-2.0% band, approximately consistent with the depreciated fair market value of mass-market seasonal home furnishings. But 159 parcels (28% of filers) declare below the 1% floor, including 31 declaring below 0.5% of assessed value.7

The non-filer cohort — non-resident-owned parcels with no PPT declaration on record — adds 335 parcels to the picture. These parcels carry no PPT at all, regardless of their current contents.

The non-filer rate is highest at the low-AV end (52% under $500K, 38% in the $500K-$1M band) and in the small high-end cohort ($4M-$6M, 57%, though the sample size of seven parcels warrants caution). 82% of non-filers (276 of 335) are in homes assessed under $1M. The compliance gap from this cohort is distributed across the lower portion of the AV distribution rather than concentrated at the top.

The two patterns — under-declaration among existing filers and non-filing among those who don’t file at all — compound with the time-lag in real estate assessment to produce a structural finding: the bulk of non-resident-owned Stockbridge residential value sits in parcels where neither the real estate assessment nor the personal property declaration has been validated against current market reality within the available transactional history. The longer the time since last arm’s-length transaction, the larger the structural gap.

The chart above contrasts two illustrative configurations. A typically-furnished seasonal home filed at the time of purchase and carried forward will declare PPT in the 1-2% of AV range — a pattern approximately consistent with the depreciated fair market value of mass-market furnishings, which is the legally taxable basis. An estate-collection home with appreciating-asset contents (antiques, original artwork, period furniture, hand-knotted rugs, sterling, fine china, mature wine collections) declared at the time of an estate transfer decades ago and carried forward will exhibit the opposite pattern: the declaration anchors to a basis that contents appreciation has since rendered substantially below current fair market value. The same 1-2% declaration pattern is approximately right for one configuration and structurally wrong for the other.

Quantifying the precise recovery available from addressing this structural pattern is outside the scope of this profile. A defensible analysis requires methodology that goes beyond the public records available here — parcel-level contents review, comparable-market documentation, and procedural engagement with the Board of Assessors. The patterns documented above identify the analytical surface area; they do not produce a recovery estimate.

Procedural tools available to towns considering action. Under M.G.L. c.59 §5 Cl.20 and the broader statutory authority over assessment and personal property valuation, a Board of Assessors has procedural options for addressing the structural lag documented above. A targeted reassessment of parcels with no arm’s-length transactional validation point in the past decade — using comparable arm’s-length sales of similar parcels as the validation basis — is the standard remedy on the real estate side. A targeted Form of List update request to high-AV non-resident parcels with declarations below the 1% sniff-test floor, paired with documentation of likely contents value, is the standard remedy on the personal property side. The Board can request copies of insurance contents schedules as supporting documentation, request professional appraisals for contested cases, and use auction-house records, gallery sale records, and qualified appraisals as the evidentiary basis for revised valuations.

The procedural tools exist. Their application requires Board of Assessors capacity and political support from the Select Board, and produces administrative and political costs that a town must weigh. The decision about whether to deploy them rests with the town’s elected and appointed officials. The empirical pattern documented above identifies the magnitude of the analytical question; the procedural response is a matter of municipal policy.

The §5C residential exemption

The §5C residential exemption is the most consequential single lever available to Stockbridge under the structural condition Chapter 4 documented. It is also the lever most directly tied to the Seasonal Community designation, the only one whose expanded form requires designation acceptance.

Mechanics. The exemption deducts a flat dollar amount from the assessed value of a qualifying primary-residence property before the property tax rate is applied. The dollar amount is set by the Town as a percentage of the average residential assessed value in town. The Town then raises the residential tax rate to recover the levy lost on exempt properties. The result: primary-resident homes pay less tax. Non-resident-owned homes pay more. Total town revenue is unchanged. The exemption is reset annually.

The exemption as structural inverse of an override. A Proposition 2½ override and a §5C residential exemption operate on the same residential tax base in structurally opposite directions. An override raises the rate proportionally across all parcels, shifting burden toward the owners with the most assessed value to tax — disproportionately non-resident-owned property in Stockbridge given the median AV differential noted in Section A3 — but raising every primary resident’s bill in the process. The §5C exemption keeps total town revenue unchanged while redistributing the tax burden specifically toward non-resident-owned property and away from primary residents. The structural effect on non-resident-owned property is similar to an override’s; the effect on primary residents is the inverse. An override raises the typical primary-resident bill. The §5C exemption lowers it. The exemption delivers a shift of burden toward non-resident-owned property without imposing a uniform rate increase on the year-round residents the changing community has most squeezed.

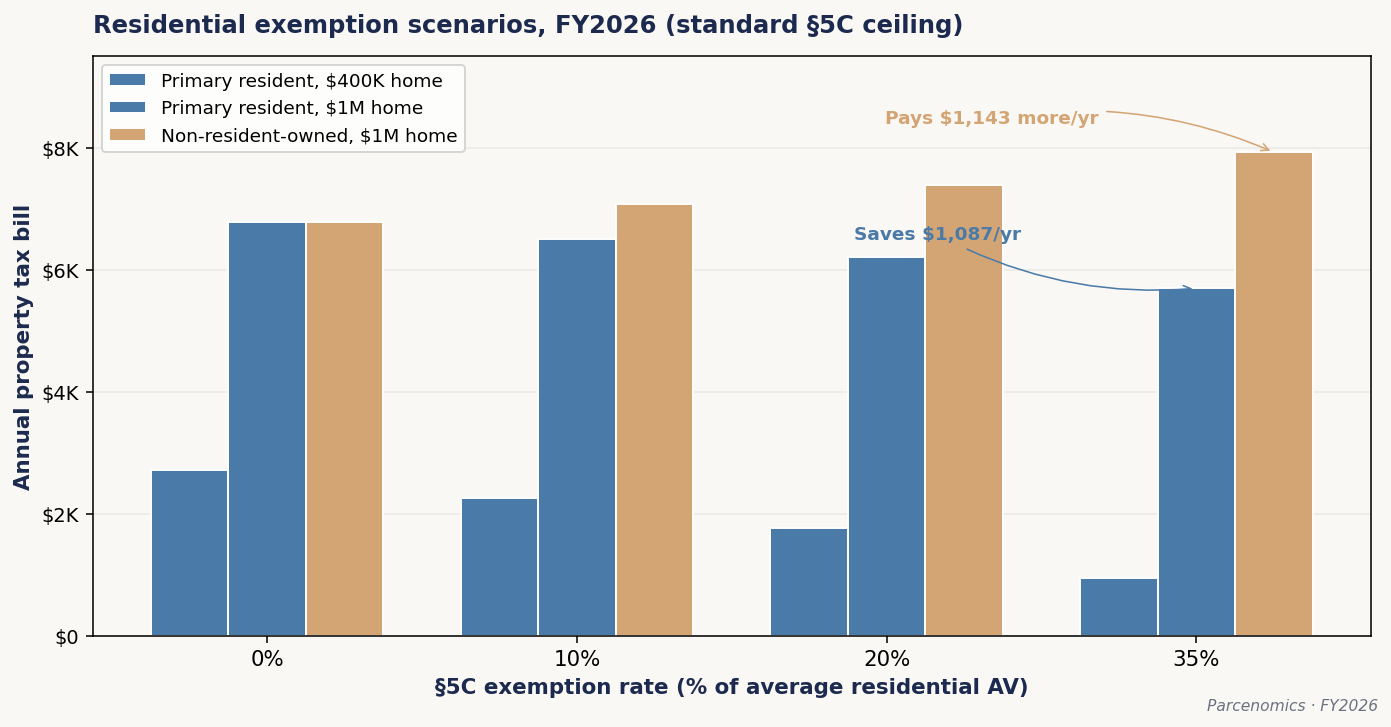

Stockbridge’s average residential assessed value is $803,059. At a 35% exemption — the maximum available under the standard §5C ceiling — every qualifying primary-residence property would have $281,071 deducted from its assessed value before the rate is applied.

The break-even point is approximately 1.5 times the town’s average residential value. A primary-residence home assessed below that point comes out ahead under the exemption — savings on the deducted assessment exceed the rate increase on the remaining assessment. A primary-residence home assessed above that point pays slightly more. Non-resident-owned homes pay the full rate increase without the offsetting deduction. They pay more at every value.

Scenarios. The locked analysis covers the standard ceiling at four exemption levels. At a 35% exemption, a primary-resident $1 million home saves approximately $1,087 per year, and a non-resident-owned $1 million home pays approximately $1,143 more.8

The 50% ceiling available to Stockbridge under the Seasonal Community designation produces a stronger version of the same effect — proportionally larger savings to primary residents below the break-even point and proportionally larger costs to non-resident-owned property. Specific 50% scenario numbers are pending a re-run of the §5C analysis under the expanded ceiling. The directional finding holds.

Stockbridge’s current posture. Stockbridge has not adopted the §5C exemption at any rate as of FY2026. Adoption of the expanded 50% ceiling requires the Town first accept the Seasonal Community designation under Section 32(b) by Town Meeting vote, then adopt the exemption at the chosen rate by Select Board action under Section 32(f). Acceptance and adoption are sequential and independent decisions, and Stockbridge is currently studying acceptance of the designation with the Berkshire Regional Planning Commission.

Stockbridge has pursued legacy-homeowner support through the senior-exemption pathway under §5 Clauses 41A, 41D, 17E, and 18 — covered in Section C. The §5C residential exemption is a separate, additional statutory mechanism the Town has not yet adopted. Both pathways exist in statute. The §5 senior-exemption suite has been the one Stockbridge has used.

Unused Proposition 2½ levy capacity

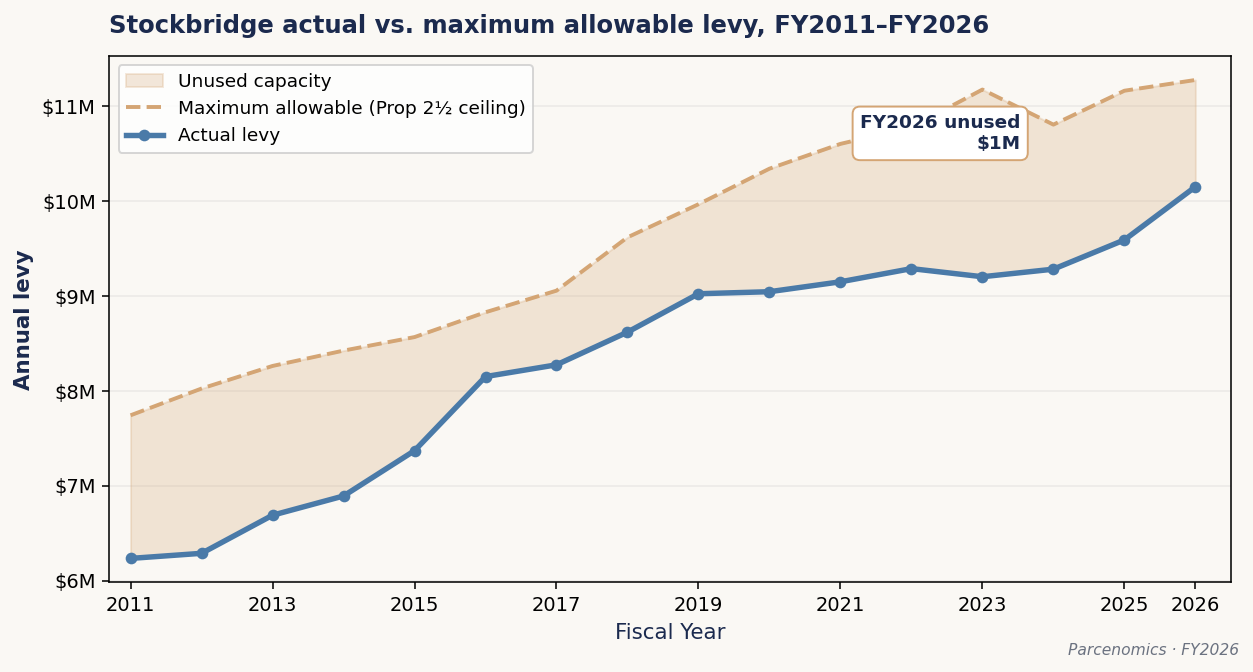

Stockbridge has $1,126,225 of unused levy capacity under Proposition 2½ in FY2026 — 9.99% of the maximum allowable levy of $11,278,372 against an actual levy of $10,152,147.9 Across the 16-year window from FY2011 to FY2026, average annual unused capacity has been $1,337,368 — about 14% of the maximum allowable. Stockbridge’s actual levy has consistently sat below the maximum allowable.

The override path — unnecessary, not blocked. Expansion of the actual levy above the existing baseline plus 2.5% annually requires a Proposition 2½ override vote at Town Meeting and the ballot box. Stockbridge has unused capacity available within the existing ceiling, tappable without any override. The override path expands the ceiling itself. The two are distinct mechanisms.

The distinction matters for how Stockbridge’s fiscal history should be read. Stockbridge has not gone to its voters for an operating override because it has not needed to. The Town has met its rising obligations, funded discretionary priorities — including approximately $1 million in borrowing to restore its Main Street monuments, a capital choice many comparable towns could not contemplate — expanded its senior-exemption parameters well beyond the statutory minimums, and stood up new programs including an affordable housing trust (funded through Community Preservation Act revenue), all while maintaining its AA+ bond rating and leaving roughly $1.1 to $1.3 million of allowable levy capacity unused each year across the 16-year record. This is the fiscal record of a disciplined, well-managed town living within its means while still funding what it chose to fund. The override has been unnecessary for Stockbridge, not blocked.

The regional override environment is relevant context, not a constraint on Stockbridge. The Great Barrington May 12, 2026 override defeat — 631 to 397, a 61% no vote — and the mixed regional results that day reflect the fiscal corner that some neighboring towns have been pushed into: obligations outrunning capacity, forcing override questions that voters then reject. Stockbridge is not in that corner. Its disciplined posture is precisely what gives it the latitude to consider the fairer, override-free tools in this chapter rather than being forced toward an override it might lose. The contrast cuts in Stockbridge’s favor: a town with room to choose its instruments, choosing among them deliberately.

Why the choice of instrument still matters. That Stockbridge has managed within its means does not make the choice of revenue instrument neutral. As the $3.9 million in new annual obligations documented in Chapter 4 arrives by FY2029, the Town will need additional revenue — and the residential property tax rate is the tool it reaches for by default. A Proposition 2½ override, were the Town ever to pursue one, raises the tax rate proportionally across all taxable parcels. In Stockbridge, the median primary-resident-owned home is assessed at approximately $588,900, producing an annual property tax bill of approximately $3,999. The median non-resident-owned home is assessed at approximately $673,650 — meaningfully higher — producing an annual property tax bill of approximately $4,574.10 An across-the-board rate increase of, for example, $0.50 per thousand of assessed value would add approximately $294 to the median primary-resident bill and approximately $337 to the median non-resident bill. In absolute dollars, more of the burden falls on non-resident-owned property — but the increase lands on every primary resident regardless of capacity to absorb it, including the fixed-income seniors and working-age households the changing community has most squeezed. The §5C exemption and the compliance levers achieve a comparable shift of burden toward non-resident-owned property without imposing a uniform rate increase on the residents least able to pay. The instrument the Town selects determines who carries the new burden, even when the total revenue raised is the same.

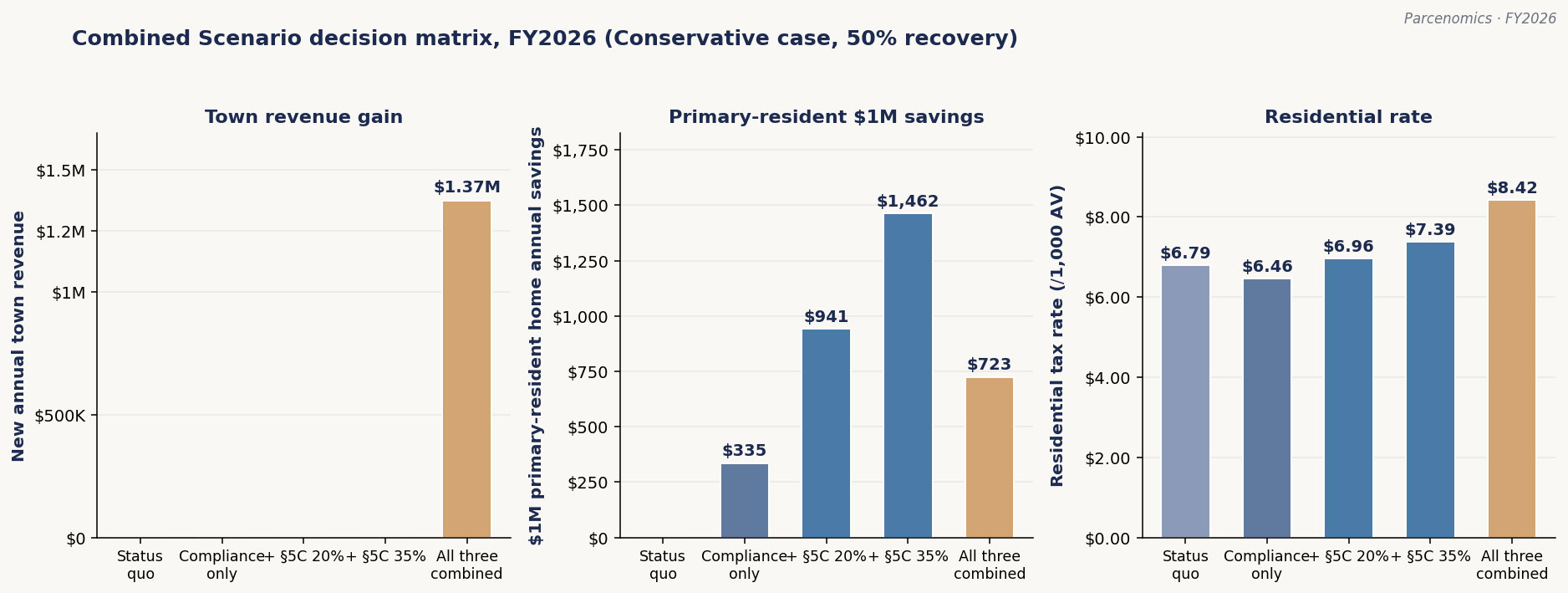

Combined Scenario — all three independent levers

The first three levers — compliance recovery, §5C exemption (at the standard 35% ceiling), and tapping the unused Proposition 2½ levy capacity — can be activated independently or in combination. The locked analysis quantifies the combination under a conservative recovery scenario.

Under a conservative recovery scenario — approximately 50% recovery on the three outreach-driven streams (personal property tax, vehicle excise, boat excise) and adoption of the short-term-rental community impact fee at the 3% statutory maximum — plus the §5C exemption at the standard 35% ceiling, plus levy expansion to the maximum allowable: combined annual town revenue gain is approximately $1,413,000. The residential tax rate moves from $6.79 to approximately $8.55. A primary-resident $1 million home saves approximately $640 per year. A non-resident-owned $1 million home pays approximately $1,760 more.11

The combined savings is smaller than the §5C-alone savings because the levy expansion in this scenario raises the residential rate, partially offsetting the exemption’s effect on the primary-resident bill. The combined cost to non-resident-owned property is larger than the §5C-alone effect because the rate increase compounds on the unprotected non-resident assessment. Both directions are consistent with the structural intent of the combined approach.

Compliance recovery operates through two distinct fiscal mechanisms. Personal property tax recovery expands the residential AV base — additional assessed value enters the levy calculation, which holds the residential rate lower than it would otherwise be at constant town revenue. The other three streams (vehicle excise, boat excise, short-term-rental community impact fees) flow as estimated receipts — direct revenue to the Town outside the property tax levy. The Combined Scenario below presents both mechanisms; the town revenue gain figure reflects estimated receipts only, while the rate effect reflects the combined operation of both buckets.

| Lever | Town revenue contribution | Effect on residential rate |

|---|---|---|

| Compliance recovery — PPT (Bucket A: AV-base expansion) | $0 | $19.7M of additional AV base producing approximately $134,000 in residential rate relief |

| Compliance recovery — vehicle / boat / c.64G §3D (Bucket B: estimated receipts) | +$287,000 | None (flows directly to town revenue) |

| §5C exemption at standard 35% ceiling | $0 (revenue-neutral) | Redistributes burden from primary-resident to non-resident-owned property |

| Levy expansion to maximum allowable | +$1,126,225 | Levy raised from $10,152,147 to $11,278,372 (Prop 2½ ceiling) |

| Combined Scenario, Conservative | +$1,413,225 | Rate $6.79 → $8.55 · $1M primary saves $640 · $1M non-resident pays $1,760 more |

The mid-case recovery scenario (60% recovery against the mid-band estimates) produces incrementally stronger numbers: approximately $1,443,000 annual gain to the Town and $658 in annual savings to a typical $1 million primary-resident home.

The combined commitments framing

The Section A levers above produce approximately $1.41 million annually in the conservative scenario. Stockbridge currently faces two near-term municipal commitments of comparable scale. The BHRSD school capital obligation, locked in November 2025 against the FY2024 EQV documented in Chapter 3, will produce debt service the Town will begin paying in the next several years. The joint Stockbridge / West Stockbridge fire-and-EMS operation, approved by voters in December 2024 and targeted for full implementation by July 2027, will produce capital and operating costs that compound through the FY2026–FY2030 transition window. The combined annual incremental burden of these two commitments is comparable in magnitude to the revenue the Section A levers would recover. The levers do not eliminate the need for these expenditures. They produce the fiscal capacity that allows the Town to meet them by distributing the new burden toward non-resident-owned property rather than spreading it uniformly across the year-round residents least able to absorb a rate increase.

The timing of lever activation relative to when the commitments come online matters. The BHRSD bond enters debt service on a schedule the school district determines. The fire station authorization is in active planning. The Section A levers can be activated incrementally — some without any vote (compliance recovery, levy capacity expansion within the existing ceiling), some on a single Select Board action (§5C exemption at the standard 35% ceiling), some on a sequential Town Meeting plus Select Board sequence (§5C expanded 50% ceiling via Seasonal Community designation acceptance). The Town has the procedural pieces to begin activation now. The fiscal effects compound year over year.

Section B — Housing Production and Demand Tools

The Seasonal Community designation under Section 32 of Chapter 150 makes a suite of housing-production and fiscal tools available to designated municipalities. Stockbridge’s posture as of the date of this profile is one of active deliberation — the Town is studying acceptance with the Berkshire Regional Planning Commission and has not brought acceptance to Town Meeting. The toolkit below would become available if acceptance is voted. The obligations that come with acceptance are described alongside the opportunities.12

The Section 32 toolkit

Discretionary tools (Section 32(d)) — may be exercised by an accepting municipality:

- Acquire year-round occupancy restrictions on housing through restriction or deed amendment.

- Acquire and develop housing for public employees of the municipality.

- Conduct biennial housing-needs assessments.

- Establish a Year-Round Housing Trust Fund.

- Establish funds for artist and literary worker housing.

- Eligibility for the Seasonal Communities Grant Program, with state grants currently capped at $175,000 per town per year.

Mandatory adoptions (Section 32(e)) — must be enacted by an accepting municipality:

- Adopt zoning bylaws permitting undersized lots for year-round housing.

- Adopt zoning bylaws permitting tiny houses for year-round residential use.

The §5C residential exemption ceiling expansion under Section 32(f), covered in Section A, is also conditional on acceptance.

The acceptance decision

Acceptance triggers both opportunities and obligations. The discretionary tools are opportunities the Town can choose to use or not after acceptance. The mandatory adoptions are zoning changes the Town must enact within the timeline the Act and the EOHLC regulations specify. The §5C 50% expansion is enabled but not required.

Whether the discretionary tools are valuable in Stockbridge’s specific context, and whether the mandatory adoptions are appropriate zoning policy for Stockbridge, are questions the Town and its planning processes are equipped to evaluate. The underlying zoning merits are not within the scope of this profile. The point worth surfacing is that acceptance is not a free option — there are obligations that come with the tools. The Town’s deliberation with the Berkshire Regional Planning Commission is the procedural posture where these trade-offs are being weighed.

Tools not contingent on designation

Several housing-related tools are available to Stockbridge regardless of Seasonal Community acceptance.

Accessory dwelling unit authorization under state law became statewide in 2024. Accessory dwelling units of up to 900 square feet are now permitted by-right in single-family residential zones across Massachusetts.

Community Preservation Act funds. Stockbridge participates in the CPA, which dedicates a portion of property tax revenue to open space, historic preservation, and community housing. Housing-creation grants are available through the existing CPA framework.

Existing zoning flexibility. Special permits and variances available through the Town’s existing zoning board mechanisms can apply to housing-creation projects within the existing bylaw.

These tools have been available to the Town throughout. None requires designation acceptance.

Section C — Legacy Resident Support

The exec summary introduced the term legacy homeowners — property-rich, cash-poor full-time residents — increasingly used in Berkshire municipal discussions to describe the population most exposed to the structural condition Chapter 4 documented. Section C examines the statutory mechanisms available to a town that wants to keep its legacy homeowners in their homes as property values appreciate around them.

The §5C exemption as a legacy-support mechanism

The §5C exemption is the principal statutory mechanism for shifting tax burden toward the population that arrived during the transformation Chapter 4 documented and away from the population whose income did not move with property values. Through the exemption, every qualifying primary-residence household receives a flat-dollar reduction in assessed value before the tax rate is applied. The mechanism is age- and income-blind. It covers all primary residences in town.

Section A above quantified the §5C exemption at the standard 35% ceiling and noted the 50% ceiling available under Seasonal Community designation. The scenarios there are the operative numbers. The framing here is the structural argument for which population the exemption protects.

Senior tax deferral and exemption

Stockbridge has adopted the full senior-exemption package available under M.G.L. c.59 §5 — Clauses 41A (senior tax deferral), 41D (senior exemption with cost-of-living adjustment, the 41C variant), 17E (widow, elderly, minor exemption with cost-of-living adjustment, the 17D variant), and 18 (hardship abatement) — as a Town Meeting package rather than as separate single-clause adoptions.13 The four clauses together form a layered support structure for older, fixed-income, and disability-impacted year-round residents. Adoption is in place. The structural question facing the Town is utilization, not adoption.

Clause 41A — Senior Tax Deferral is the most powerful of the four. A qualifying senior may defer payment of all or part of their annual property tax bill. The deferred amount accumulates as a lien against the property repayable from the eventual sale or transfer. The deferral allows a property-rich, cash-poor senior to remain in their home through retirement years when income is fixed and property tax bills rise with assessed value. Two operative parameters set by Town Meeting determine the practical reach of the clause:

- Income ceiling. Stockbridge’s adopted income ceiling is $75,000 — the 2025 state Circuit Breaker non-head-of-household income limit. The statutory minimum is $20,000.

- Interest rate on deferred amounts. Stockbridge’s adopted interest rate is 5%. The statutory default is 8%; municipalities may adopt a lower rate by Town Meeting vote. The rate increases to 16% upon sale, transfer, or death of the deferring taxpayer.

Both parameters were deliberately expanded by Town Meeting vote in FY2024. The income ceiling moved from the $20,000 statutory minimum to $75,000, broadening eligibility to a substantially larger share of fixed-income seniors. The interest rate dropped from the 8% statutory default to 5%, reducing the long-term cost to a deferring household. The combined effect is a senior-deferral program that reaches well beyond what the statutory minimums would support.

Clause 41D — Senior Exemption (with cost-of-living adjustment). Provides a flat-dollar exemption on the current-year property tax bill for qualifying seniors meeting income and asset tests. Unlike Clause 41A, which defers tax to a future sale, Clause 41D reduces the current-year bill outright. Stockbridge’s adopted exemption amount is $1,000 per qualifying household per year. The FY2026 income limits are $27,475 (single) and $31,705 (married), with statutory Social Security deductions applied per DOR rules. The asset limits are $59,183 (single) and $63,409 (married).

Clause 17E — Widow, Elderly, Minor Exemption (with cost-of-living adjustment). Provides a fixed exemption to surviving spouses, elderly residents, and minor children of deceased property owners under specified conditions. Stockbridge’s adopted exemption amount is $426 per qualifying household per year. There is no income limit under Clause 17E. The asset limit is $84,548 (single or married).

Clause 18 — Hardship Abatement. Authorizes the Board of Assessors to grant case-by-case abatements for taxpayers experiencing financial hardship. Adoption is in place. No applications have been received in recent years. Whether this reflects absence of qualifying hardship or absence of program awareness is not measurable from the available data.

The four clauses adopted together represent the most thorough senior-support posture available under the §5 framework, with both 41A and 41D extended materially beyond statutory minimums. The structural question facing the Town is whether the operative parameters reach the legacy homeowners the clauses are designed to support, and whether utilization tracks eligibility. The first question is answerable by Town Meeting review of the parameter values. The second question is answerable by Board of Assessors data on application rates, where that data is collected and surfaced.

The unaddressed gap — entry-level affordability for the next generation

The senior-exemption suite and the §5C residential exemption are both retention tools. They lower the carrying cost of a home for a household that already owns one — the senior aging in place, the primary resident protected from the rate increase that funds the exemption. They are the right tools for the population they serve, and Stockbridge has adopted them about as fully as the statute allows. But retention is only half of what a year-round community needs to sustain itself. The other half is entry: the ability of the next generation of year-round households — the working-age families who would staff the institutions, fill the volunteer roles, and enroll children in the schools — to acquire a home in town in the first place. Nothing in the toolkit Stockbridge has adopted addresses entry.

This gap has a fiscal dimension that is worth naming plainly. A senior exemption is financed through an overlay: the revenue the Town forgoes on exempt senior households is recovered by raising the residential rate on every non-exempt household. Among those non-exempt households are the working-age, year-round residents whose incomes have not tracked the property-value transformation Chapter 1 documents. The Town’s most developed equity intervention is, in part, carried by the very cohort that faces the next affordability problem and has no comparable mechanism addressing it. This is not an argument against senior relief, which is sound policy for a vulnerable population. It is an observation that the Town has built one half of a generational strategy and not the other, and that the half it has built is partly financed by the half it has not.

The boards that expanded Stockbridge’s senior-exemption parameters and stood up its affordable housing trust did real and prudent work. But that work has not been coupled with a mechanism for entry-level homeownership, and the consequence is visible across the demographic record assembled in this profile: an aging year-round population (54.3% age 65 or older per Chapter 1), a shrinking under-35 cohort, new buyers who do not convert to year-round primary residency at the rates the conversion analysis would predict, and a median-household-income trajectory driven by the in-migration of higher-income households rather than rising incomes among the families already here. Each of these is a symptom of the same underlying condition: a community that has built well for the residents it has and aging, without building a path for the residents it needs next.

The tools that would address entry are not in Section A or Section C. They are in Section B — the housing-production tools the Seasonal Community designation unlocks. The Section 32(d) discretionary tools (year-round occupancy restrictions, a Year-Round Housing Trust Fund capitalized beyond what CPA alone can fund, public-employee housing), the Section 32(e) zoning adoptions (undersized lots, tiny houses for year-round use), the statewide accessory-dwelling-unit authorization, and the existing CPA housing-creation framework are the supply-and-entry instruments that the fiscal and retention levers do not touch. This profile does not prescribe which of them Stockbridge should adopt; the Section 32 mandatory adoptions in particular carry real zoning trade-offs the Town and its planning processes are equipped to weigh, and the merits of any specific zoning change are outside this profile’s scope. The point is narrower and structural: the retention half of the strategy (Sections A and C) and the entry half (Section B) are two halves of one generational problem, and the data shows Stockbridge has advanced the first without yet engaging the second.

Fiscal tools and legacy support as one strategy

The Section A levers and the Section C legacy-support mechanisms are two halves of one fiscal strategy. The Section A levers generate the revenue and the rate-structure shift that fund a proactive response to the structural condition Chapter 4 documented. The Section C mechanisms — the §5C residential exemption and the §5 senior-exemption package — protect the legacy homeowners the structural condition has most exposed.

The §5C residential exemption (Section A and Section C1) covers all qualifying primary residences regardless of age or income. It operates at the scale of the residential tax base. The §5 senior-exemption package (Section C2) covers seniors and limited-income or hardship-impacted year-round residents specifically. It operates at the scale of qualifying individuals. The two mechanisms are complementary, not redundant. Both are retention mechanisms; as the preceding section notes, the entry side of the strategy lives in the Section B housing-production tools.

The fiscal-tools analysis in Section A is calibrated against the combined annual incremental burden of the BHRSD school capital obligation and the anticipated fire station debt exclusion that Chapter 3 documented. The Section C legacy-support mechanisms are calibrated against the structural condition Chapter 4 documented — the demographic transformation that has compressed the year-round community and concentrated its tax burden on a fixed-income, aging population.

The timing matters. Lever activation that compounds for several years before the major commitments come into full effect produces a meaningfully different fiscal posture than activation that begins after. The Town has the procedural pieces to begin activation now. The decisions are the Town’s to make.

Footnotes

- Compliance recovery analysis: packet 4a (outreach candidates plus per-stream gap estimates) at outputs/v8_session2_packets/chapter5/. Methodology and per-parcel outreach candidate identification documented in the Technical Appendix. Aggregate annual gap estimates use mid-band recovery rates of 50% (Conservative case) and 60% (Mid-case) against per-stream identified candidate universes. ↩

- Personal property tax non-filer identification: 247 candidates identified as a strict universe — residential parcels classified as non-resident by the residency tier model (medium or high confidence, manual overrides applied) whose owners are not currently on the FY2026 personal property roll. The 247 cohort excludes approximately 24 additional parcels in the contested-signal and unresolved entity-owned tiers, which are deferred to subsequent residency-classifier refinement and would expand the recoverable universe if their classification firms up. Per-parcel outreach methodology and candidate list detailed in the Technical Appendix. ↩

- Vehicle excise recovery candidate identification: 117 non-resident-owned parcels within a 300-mile radius with vehicle-garaging signals consistent with Stockbridge use. Methodology and candidate list documented in the Technical Appendix. ↩

- Boat excise recovery candidate identification: 452 parcels with mooring, dock, or boat-storage signals and no boat excise filing on record. Methodology documented in the Technical Appendix. ↩

- M.G.L. c.64G §3D(a) authorizes a community impact fee of up to 3% on professionally-managed short-term rentals; M.G.L. c.64G §3D(b) provides for a separate vote to extend the fee to owner-occupied two- and three-family dwellings operating as STRs. Stockbridge has not adopted either provision — FY2026 Tax Rate Recapitulation, Page 5 (Local Receipts Not Allocated) line 10b shows $0 actual and $0 estimated for “Community Impact Fee Short Term Rentals.” Estimated revenue at 1%, 2%, and 3% adoption rates derived from packet 4a STR base projection (approximately $4.7 million estimated STR-attributable lodging activity in Stockbridge based on FY2026 room excise volume). M.G.L. c.64G §3D(c) requires that at least 35% of receipts be dedicated to affordable housing or local infrastructure; the remaining 65% is unrestricted general revenue. ↩

- Time-lag stratification: parcel-level analysis of the FY2026 non-resident-owned residential cohort against the 20-year sales register. Arm’s-length filtering applied per Massachusetts Department of Revenue conventions (excludes family transfers, foreclosures, distress sales, $0 and $1 deeds, government transfers). Cohorts: arm’s-length sale in last 10 years (180 parcels, $169M AV); non-arm’s-length transfer only in last 10 years (141 parcels, $159M AV); no transfer of any kind in 20-year register (577 parcels, $480M AV). Total: 898 parcels, $808M AV. Sales register depth: earliest sale September 2005, latest March 2026. ↩

- PPT declaration ratio: declared total appraised PPT divided by assessed value, computed across the 563 non-resident-classified residential parcels with current PPT declarations on file. Mean 1.55%, median 1.23%, distribution: 31 parcels below 0.5% of AV, 128 between 0.5% and 1.0%, 387 between 1.0% and 2.0%, 17 above 2.0% (including 10 above 10% that appear to be data-quality outliers). PPT declarations summed across multiple accounts at the same situs address. ↩

- §5C residential exemption mechanics: M.G.L. c.59 §5C. Per-parcel exemption equals the exemption-percentage times the average residential assessed value (FY2026 Stockbridge: $803,059). The residential tax rate is recalibrated annually to recover the levy lost on exempt properties. Scenario figures apply to the 698 primary-resident parcels in Stockbridge as identified by the residency tier classifier (see Chapter 2 Note 12); the same FY2026 residential levy of $9,247,901 is redistributed across non-exempt assessment. The 35% ceiling figures cited in this section are the operative analytical values; 50% ceiling figures are pending re-run under the Seasonal-Community expanded ceiling. ↩

- Unused Proposition 2½ levy capacity from packet 4c (FY2011–FY2026 levy limit reconstruction against DOR-certified Levy Limit form data). FY2026: maximum allowable levy $11,278,372, actual levy $10,152,147, unused capacity $1,126,225 (9.99% of max). 16-year mean unused capacity $1,337,368 (14.03% of max). Narrowest year FY2016 ($678,594 unused, 7.69%); widest year FY2023 ($1,973,991 unused, 17.66%). ↩

- Median residential tax bills by residency tier computed from the FY2026 assessor records using the residency tier classifier. Median assessed value among primary-resident-classified residential parcels: $588,900 (n=698). Median assessed value among non-resident-classified residential parcels: $673,650 (n=898). Residential rate FY2026: $6.79 per $1,000 of assessed value. The hypothetical override increment of $0.50 per $1,000 is illustrative; actual override magnitudes vary. ↩

- Combined Scenario figures from packet 4d, Conservative case assumptions: 50% recovery on the three outreach-driven compliance streams (personal property tax, vehicle excise, boat excise) against per-stream mid-band gap estimates; adoption of the M.G.L. c.64G §3D short-term rental community impact fee at the 3% statutory maximum; §5C residential exemption adopted at the standard 35% ceiling; Proposition 2½ levy expanded from $10,152,147 actual to $11,278,372 maximum allowable. Decomposition of the $1,413,225 town revenue gain: $1,126,225 from levy expansion plus $287,000 from estimated-receipts compliance (vehicle excise, boat excise, and c.64G §3D community impact fees, which flow outside the property tax levy as direct revenue to the Town). Personal property tax compliance recovery ($134,000 at 50% recovery against the strict-universe 247-parcel insurance-replacement estimate; AV-base expansion of approximately $19.7 million at the FY2026 residential rate) operates as residential rate relief through AV-base expansion rather than as direct town revenue. The §5C exemption at 35% is revenue-neutral. Mid-case recovery scenario assumes 60% recovery on the three outreach streams (other assumptions unchanged): town revenue gain approximately $1,443,000, primary-resident $1 million home savings approximately $658, non-resident $1 million home extra cost approximately $1,740, residential rate approximately $8.53. Full per-stream methodology documented in the Technical Appendix. ↩

- Section 32 of Chapter 150 of the Acts of 2024 (the Affordable Homes Act), codified at M.G.L. c.23B §32. Discretionary tools enumerated in Section 32(d); mandatory adoptions in Section 32(e); residential exemption ceiling expansion to 50% in Section 32(f). Seasonal Communities Grant Program eligibility limit per the December 2025 grant round announcement from the Executive Office of Housing and Livable Communities. ↩

- M.G.L. c.59 §5: Clause 41A (senior tax deferral), Clause 41D (senior exemption with cost-of-living adjustment, the 41C variant), Clause 17E (widow / elderly / minor exemption with cost-of-living adjustment, the 17D variant), and Clause 18 (hardship abatement). Stockbridge accepted all four clauses by Town Meeting vote. Operative parameters confirmed by the Stockbridge Board of Assessors (Senior Property Tax Exemption Guidelines for Income & Equity, FY2026 schedule): Clause 41A income ceiling $75,000 (the 2025 state Circuit Breaker non-head-of-household income limit), interest rate on deferred amounts 5%; both parameters expanded by Town Meeting vote in FY2024 from statutory minimums of $20,000 income ceiling and 8% interest rate respectively. Clause 41D exemption amount $1,000 per qualifying household per year; income limits $27,475 (single) and $31,705 (married) with statutory Social Security deductions applied; asset limits $59,183 (single) and $63,409 (married). Clause 17E exemption amount $426 per qualifying household per year; no income limit; asset limit $84,548 (single or married). Clause 18 hardship abatement is granted at the discretion of the Board of Assessors; no applications have been received in recent years. ↩